Millions of Americans living in wildfire-prone areas have homes that are not constructed with wildfire in mind. Roofs are highly vulnerable to wildfire due to their large surface area and potential for embers to accumulate. Understanding how many vulnerable roofs exist in wildfire-prone areas can illuminate the scale and cost of home retrofits needed to help communities adapt to wildfires.

In this study, we analyze roofing data from Zillow’s Transaction and Real Estate Database (ZTRAX) and wildfire risk data from U.S. Forest Service’s Wildfire Risk to Communities. We find that of the 41 million buildings in the United States with roof attribute data, nearly 1 million have combustible wood shake or shingle roof coverings in areas of medium to very high (40th percentile or above) wildfire risk. We estimate retrofitting these roofs would cost a minimum of $6 billion. This is likely a significant underestimate as roofing data was available for fewer than a quarter of homes and roof replacement costs were estimated conservatively.

Roofs are just one component of the home mitigation needed to help communities survive wildfires. The funding needed for roofs alone dwarfs the current funding available for community wildfire resilience.

Building materials influence home survival

Home and property mitigation can influence whether a structure survives a wildfire. “Hardening a home” against increasing wildfire risks—that is, modifying the home’s design, layout, building materials, and near-home landscaping—will reduce its vulnerability to embers, radiant heat, and flames.

While the roof is only one assembly to consider when evaluating the vulnerability of a home, assessing roof coverings communitywide can provide insights to the scale and scope of community retrofitting needs, relative susceptibility, and level of investment needed to mitigate risk. Roofs are an indicator of the overall challenge of wildfire retrofits.

Analyzing roofing material and wildfire risk

This study analyzed building attribute data from Zillow’s Transaction and Real Estate Database (ZTRAX) and wildfire risk data from Wildfire Risk to Communities to better understand the scale and distribution of roof covering material in wildfire-prone areas. While ZTRAX is the most comprehensive building and property database available, there are gaps in consistency and completeness. Of the 168 million buildings included in the dataset, fewer than a quarter (40.6 million buildings) were assessed for roof covering so the results presented here are a significant undercount.

We also considered roofing materials and their structural ignition potential. Roofing materials can be noncombustible (e.g., standing seam steel), fire-resistant (e.g., asphalt fiberglass composition shingles), or combustible (e.g., wood shake/shingles). See complete Methods and Data Sources below.

Wood roofs represent a substantial challenge

Our analysis finds that asphalt composition shingles—which, with a Class A fire rating, are wildfire-resistant—are the most common roofing material today, accounting for the vast majority (78.6%) of the assessed buildings. Noncombustible roof coverings such as steel panels and tile (flat and barrel) comprised 15.6% of the assessed roofing material. Wood roofs, the most vulnerable to wildfire, comprise 5.8% of total assessed buildings.

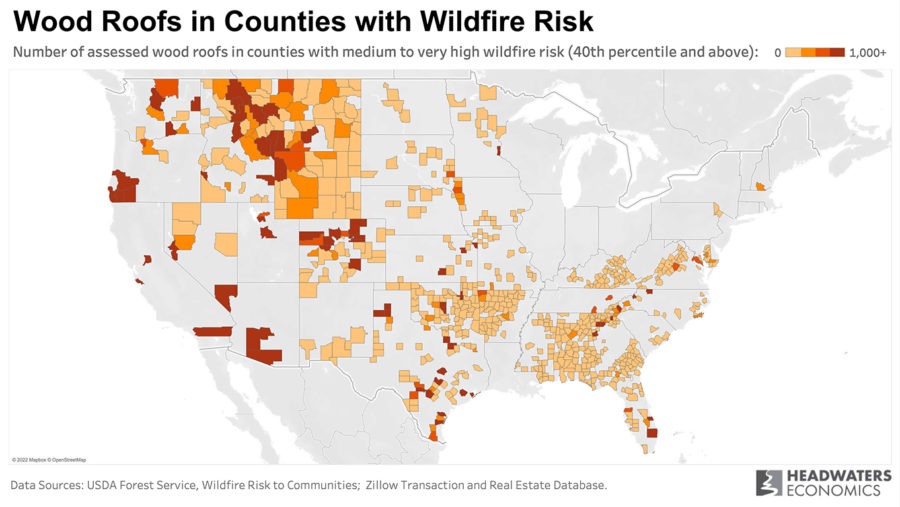

We find 1.2 million assessed buildings with wood shake/shingle roof coverings. Of these, nearly 1 million buildings were in areas with medium to high wildfire risk. The map below shows counties with wildfire risk and a large number of assessed wood roofs.

Roofing trends vary over time

Trends in roof covering materials shift over time and reflect local and regional availability, homeowner preferences, and market trends. For example, tiled roofing (with installed ventilation) is more common in warmer and drier climates where it provides thermal advantages over other types of roofing.

Asphalt fiberglass composition shingles are the most common roof covering. Since the 1960s, there has been a gradual decline in asphalt shingles as noncombustible materials such as steel and tile have become more popular. The use of wood shake/shingle roofs peaked during the 1970s and 1980s, and since the 2010s wood roofs have averaged less than 2% of the building stock. Roof material trends over time indicate an increasing preference for noncombustible materials and decreasing use of wood and asphalt-based shingles.

Counties with a high proportion of buildings with wood shake/shingle roofs and high wildfire risk should be prioritized for mitigation measures. For example, Sacramento County, California, has greater wildfire risk than 65% of other counties and has nearly 205,000 buildings with wood shake/shingle roofs, or 42% of the assessed building stock.

Our analysis found communities in nearly every part of the United States with large numbers of buildings with wood shake/shingle roof coverings and wildfire risk. For example:

- Teton County, Wyoming, on the outskirts of Yellowstone National Park, had 4,300 buildings (25% of housing stock) with wood shake/shingle roofs and has a wildfire risk higher than 87% of the country.

- Okaloosa County, Florida, on the Gulf Coast, had 42,000 buildings (52% of housing stock) with wood shake/shingle roof coverings and has a wildfire risk higher than 72% of the country.

- Lyon County, Nevada, near Reno in western Nevada, had nearly 18,000 buildings (86% of housing stock) with wood shake/shingle roofs and has a wildfire risk higher than 92% of the country.

Most of the assessed buildings across the United States had an asphalt fiberglass composition shingle roof covering, which has a Class A classification. Some counties in the country have a large proportion of buildings built with noncombustible materials such as metal and concrete. For instance, in Washoe County, Nevada, which has a greater risk than 84% of other counties in the country, nearly 31% of the assessed building stock has a noncombustible roof covering.

Explore wildfire risk and roofing material in the data visualization below.

Reducing home vulnerability requires a holistic approach

Although roofs are a primary vulnerability of a home to wildfire, it is only one of the home’s components that should be considered in the face of increasing wildfire risks. Other structural assemblies and materials influence the home’s vulnerability, including the vents, eaves, decks, near-home landscaping, and broader vegetation management and location of other combustibles around the property.

This analysis does not consider complex roof designs and other features of the roof (e.g., the roof edge) that can influence building vulnerability to wildfire. Embers can accumulate at roof-to-wall intersections (such as where roof covering meets siding of dormers), roof valleys, and in gutter systems. If not properly mitigated—for example, installing metal flashing at roof-to-wall intersections and valleys, or using noncombustible siding and gutter systems—the roof and building are still vulnerable to ignition. It is therefore important to holistically consider home mitigation through multiple coordinated efforts.

Invest in wildfire-resistant homes and communities

The large percentage of wildfire-resistant roof coverings, including asphalt fiberglass composition shingles and steel panels, suggests that retrofitting vulnerable roofs can be targeted, strategic, and cost-effective. Counties with wood shake or shingle roofs and medium to high wildfire risk should be prioritized for mitigation projects and funding.

Replacing vulnerable wood roofs will cost at least $6 billion

Funding to replace wood shake and shingle roof coverings is needed to incentivize homeowners and neighborhoods to take action. Estimated costs for installing a Class A asphalt fiberglass composition shingle roof on a typical home (e.g., simple roof design, two-bedrooms, attached garage) ranges from $6,000 to $10,000. For a noncombustible roof covering, such as standing seam metal panels or tile, costs are approximately $15,000 to more than $20,000, depending on the home design, square footage, supplier, location, and other factors.

Replacing the existing 1 million wood-covered roofs in wildfire risk areas with a Class A classification roof covering, such as asphalt fiberglass composition shingles, requires a minimum investment of $6 billion nationally. This is likely a conservative estimate of the true costs of roofing retrofits.

Funding programs should target wildfire-resistant retrofits

Ensuring that homes in wildfire-prone areas are built to resist wildfires requires a deliberate investment in communities by state and federal governments on a scale not yet seen. The 2021 Infrastructure Investment and Jobs Act (IIJA) is a step in the right direction and includes $1 billion for a new Community Wildfire Defense Grant (CWDG) program. This represents a significant opportunity and should be used to fund home hardening.

FEMA’s Building Resilient Infrastructure and Communities (BRIC) grant program is another opportunity, with over $1 billion in funding in FY2021. However, building retrofits for wildfire do not fit easily within BRIC’s priority funding areas.

Both BRIC and CWDG are competitive programs, which can be difficult for rural and low-capacity communities to access. Further, FEMA funds have typically benefitted higher-capacity coastal states, and grant requirements such as benefit-cost analyses can be barriers for rural and lower-income communities.

New programs are needed, especially to support retrofits for low-income, elderly, and other socially vulnerable residents. For example, a new partnership between California and FEMA creates a $100 million home-hardening program. With a pilot project in San Diego County, it could serve as a model for other communities. But with retrofits for wooden roofs alone surpassing a $6 billion price tag, more funding is needed to help communities replace and install building materials, develop infrastructure, and conduct long-term planning.

Adopting building codes today will help tomorrow’s wildfire resilience

Adopting and enforcing building codes requiring Class A fire-rated roof coverings and other home and property mitigation measures is another important step in reducing overall community wildfire risk. Home and property wildfire mitigation strategies are most effective when every home in the neighborhood participates. A homeowner may incorporate every recommendation to make their house less vulnerable to ignitions, but one neighbor’s inaction can still present a threat to nearby homes. This can be of particular concern for dense developments and when homes are closely situated. Policies mandating broad compliance with wildfire-resistant construction and mitigation measures can reduce community vulnerability to wildfires.

Constructing a wildfire-resistant home will improve the chance of home survival but it is not a guarantee. Complementary mitigation measures such as reducing the continuity of fuels around the home, ensuring broad neighborhood compliance, and continually maintaining the home and property are essential.

With increasingly devastating wildfires, now is the time to invest in community resilience. We need to adopt more cost-effective and proactive risk-reduction strategies that anticipate the inevitable occurrence of wildfires. Given the increasing risk of wildfires, significant additional funding is needed to help communities replace and install building materials, develop infrastructure, and conduct long-term planning.

Methods and Data Sources

Roof Covering Data

Housing attribute data identifying roof covering material was provided by the Zillow Transaction and Assessment Dataset (ZTRAX). ZTRAX is the country’s largest real estate database made available to U.S. academic, nonprofit, and government researchers. ZTRAX includes housing data for more than 3,000 counties and includes tax assessment details (parcel numbers, sale information, owner names, etc.) and transaction data (sale dates, property characteristics, geographic information, etc.).

For this research, the ZTRAX Roof Cover Standard Code field was used to tabulate assessed roof covering material across the country. A majority of recorded properties in the database did not include roof covering material and were therefore omitted from analysis. Of the 168 million buildings included in the dataset, fewer than a quarter (or 40.6 million buildings) were assessed for roof covering.

For assessed properties, roofs were coded by material with a total of 22 different roof material types. Roof codes were then clustered into one of four primary ratings:

| Roof covering type | Description | Cluster name |

|---|---|---|

| Combustible | Burnable | Wood |

| Class A combustible components | Class A classification roof coverings that have combustible components including those that attain the fire rating through the use of an additional fire-resistant underlayment. | Wildfire-Resistant |

| Class A noncombustible components | Highest rating offering the best performance to fire. | Noncombustible |

| Other | Material not considered combustible or Class A classification roof coverings (such as Class C classification) and/or unknown | Other |

Wildfire Risk Data

Wildfire risk is based on the metric “Risk to Homes” (also called “Risk to Potential Structures”) from Wildfire Risk to Communities, a project of the USDA Forest Service Washington Office of Fire and Aviation Management created in partnership with USDA Forest Service Rocky Mountain Research Station’s Missoula Fire Sciences Laboratory, Pyrologix, and Headwaters Economics.

On the map, wildfire risk is shown relative to the entire nation. Wildfire risk is binned into five classes, as per guidelines in the publication accompanying the dataset.

- Low: 1 to 40th percentile

- Medium: 40th to 70th percentile

- Medium-High: 70th to 90th percentile

- High: 90th to 95th percentile

- Very High: 95th to 100th percentile

Acknowledgments

Dr. Stephen L. Quarles contributed to this analysis.